A number of international organizations are voicing their concerns about rising inequality and precarious forms of work. A recent report from the International Monetary Fund (IMF) warned of the negative impacts of some neoliberal policies for inequality and growth. The 2016 World Economic Forum Global Risk Report notes that excessive inequality lowers aggregate demand and threatens social insecurity. And in a 2015 report, the OECD noted that the growth in non-standard jobs is a key factor contributing to rising inequality in OECD countries, including Canada.

Precarious work – temporary employment, part-time work, on-call shifts and instability – is increasingly prominent in today’s labour market. For example, at least 20% of those working in Canada are in precarious forms of employment – and this type of employment has increased by nearly 50% in the last 20 years.

Not surprisingly, growing employment precarity has been coupled with wage stagnation. From 1981 to 2011, Canadian real GDP per person grew by 50%, but the real median hourly wage rose by just 10% over the same period.

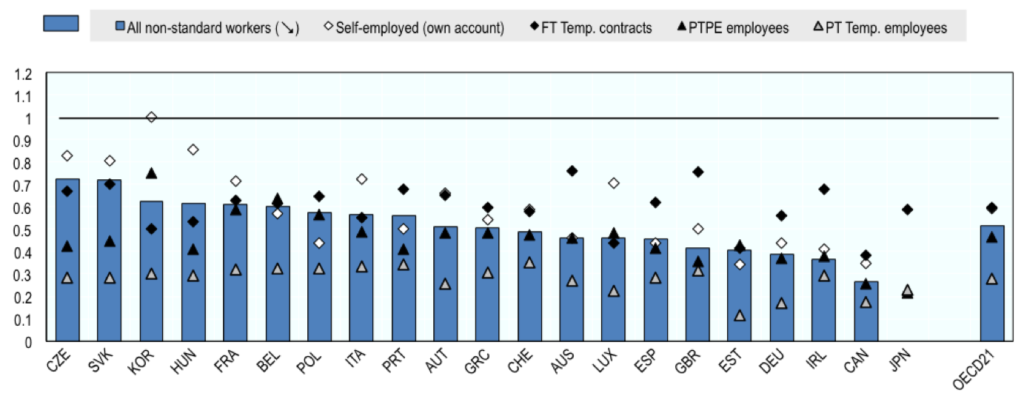

Recent research conducted by the OECD is particularly telling. The OECD found that the pay gap between “standard” workers – those in full-time open-ended contracts – and non-standard workers – workers in temporary work, part-time work or self-employment – is wide, particularly in Canada. While a non-standard worker in the OECD earns on average 75% of the hourly wage of a standard worker, she earns only 57% of a standard wage in Canada.

Chart 1: Median Hourly Earnings for Standard and Non-Standard Workers

Source: OECD, 2015, In It Together: Why Less Inequality Benefits All…in Canada

Canada has the highest rate of poverty for non-standard workers among OECD countries.

This is a grim reality for the workers that are faced with it. It’s a concern for labour, it’s a concern for economists, and it’s a concern for public policymakers.

It is also a concern for investors.

There are two principal areas of concern for investors: impacts on the economy, and impacts on the firm.

Too often investors are narrowly focused on the firm, and not on the portfolio as a whole. But weak economies drag down performance across the board. And economies are weakened by increased poverty, the evisceration of the middle class and the growing disparity between the very rich and the middle and lower classes.

One of the ways that economies are weakened is through the harmful effects of growing inequality for long-term economic growth. The OECD estimates that the rise of income inequality between 1984 and 2004, for example, knocked 4.7 percentage points off the OECD countries’ cumulative growth, on average, between 1990 and 2010. That is, rather than a cumulative growth of 33%, the 19 OECD economies saw growth of 28%. That’s a huge difference.

At the company level, more research is showing the impacts of growing inequality and precarious work on business outcomes.

For example, a study by MSCI released in April found that between 2009 and 2014 companies with lower intra-corporate pay gaps performed better in terms of average profit margins across all sectors except Materials. The study also shows that labour productivity, measured by sales per employee, was lower for companies with high intra-corporate pay gaps on average in the majority of sectors.

Companies with high levels of precarious work and poor labour practices can also experience problems such as high turnover and lower productivity, which in turn contribute to poorer levels of service, customer satisfaction and sales.

Let’s consider a concrete example from the retail sector. One of the challenges that retail companies face in managing their inventories is phantom stockouts. A phantom stockout is when a product ends up somewhere in the store where neither the customer who wants to buy it nor the employee trying to help, can find it. Phantom stockouts are a major source of lost sales, wasted productivity and reduced margins for retail businesses. Research and analysis conducted by Zeynep Ton, MIT Professor and author of The Good Jobs Strategy, found that in the retail sector one of the key factors leading to phantom stockouts was that companies were not only understaffing but also failing to invest in their employees. She found that stores with high employee turnover, less training, and greater workload experience this problem more often.

On the other hand, there are several ways that valuing workers helps business performance. For example, strong workplace practices help companies attract stronger candidates and retain key employees leading to lower turnover and retraining costs.

Good training programs and strong human resource policies can also improve employee productivity, operational efficiency, brand value, and sales. Borrowing again from the excellent work of Zeynep Ton, she has found that in the retail sector, companies that are following a Good Jobs Strategy are more likely to improve store execution, manage inventory more efficiently and deliver stronger performance.

So how are Canadian companies investing in their workers? The short answer is we really don’t know because Canadian companies are not reporting fully and reliably on a set of decent work metrics that would allow investors to truly gauge how they’re doing.

For Canada’s largest employers, retail companies, human capital reporting is mostly window dressing. Some report OHS metrics such as lost-time injuries and accident severity rates but little else; some report the number of employees that participate in training and mentor programs. A few provide data on the number of full-time versus part-time employees.

Canadian companies need to provide much better disclosure in areas such as workforce composition, retention and turnover rates, compensation levels, benefits, and workplace diversity. In addition to these metrics, company approaches to scheduling, and internal promotion rates are particularly important for addressing the question of precarious employment.

But companies are not going to report these metrics if investors are not demanding them. Despite a growing body of evidence that human capital policies can be material to corporate performance, investors presumably still accept the narrative that employees are a cost to be minimized and not an asset to be invested in.

And that’s why we at SHARE are very excited to have launched a new project with the Atkinson Foundation called “Valuing Decent Work”. The project will mobilize investors to advocate for robust decent work policies and practices in investee companies by demonstrating the importance of decent work for company performance, value creation and in building a sustainable and resilient Canadian economy.

We are going to be working with investors to break the silence around decent work in corporate reporting; to change the narrative from workers as a “cost”, to workers as a “driver of value”; and to identify the right metrics to drive change and measure success.

Broadbent Institute, 2014, Haves and Have-Nots: Deep and Persistent Wealth Inequality in Canada, https://d3n8a8pro7vhmx.cloudfront.net/broadbent/pages/32/attachments/original/1430002827/Haves_and_Have-Nots.pdf?1430002827

OECD, 2015, In It Together: Why Less Inequality Benefits All, http://www.keepeek.com/Digital-Asset-Management/oecd/employment/in-it-together-why-less-inequality-benefits-all_9789264235120-en#page4.

MSCI, 2016, Income Inequality and the Intracorporate Pay Gap, https://www.msci.com/www/research-paper/income-inequality-and-the/0337258305.