Executive Summary

At first glance, most Canadian companies appear to have a choice when it comes to climate disclosures. Outside the federally regulated financial services sector, climate disclosure remains voluntary for listed companies, despite the fact that Canadian Sustainability Disclosure Standards – CSDS 1 and CSDS 2, Canada’s version of the International Sustainability Standards Board’s (ISSB) global climate-reporting baseline – have been finalized as of December 2024, effective January 1, 2025.

In practice, however, climate disclosures are not really optional, and Canada’s failure to require mandatory climate disclosures isn’t sparing Canadian companies – it’s penalizing them.

Within and outside Canada, companies are being required to provide rigorous climate-related disclosures to lenders, insurers, trading partners and overseas regulators, including, but not limited to:

- Office of the Superintendent of Financial Institutions’ Guideline B-15: guideline requiring Federally regulated Canadian banks and insurers to collect and report climate-related information about their counterparties;

- EU’s Corporate Sustainability Reporting Directive (CSRD): robust sustainability disclosure requirements apply to Canadian parent companies that meet EU turnover and operational thresholds. These requirements apply to companies’ entire global business, not just their EU activities;

- Carbon Border Adjustment Mechanism (CBAM – EU and UK): regulations attaching a carbon cost to imports of cement, iron and steel, aluminium, fertilizers, electricity, and hydrogen, requiring Canadian exporters in these sectors to report verified emissions data;

- California State Bills 253: emissions disclosure requirements extending to out of state companies doing business in California above a certain threshold, with Canadian suppliers impacted indirectly via expanding requirements starting 2027;

- EU’s Capital Requirements Regulation (CRR3) and UK Prudential Regulation Authority’s Supervisory Statement 5/25: parallel obligations on EU and UK banks and insurers to collect and report climate-related information about their counterparties.

In the absence of company-specific climate disclosures, lenders, insurers, and trading partners fall back on sector and regional averages which can substantially overstate emissions for cleaner-than-average producers, including many Canadian companies operating on clean grids or using advanced production methods. This results in Canadian companies facing a competitive disadvantage, inflated risk estimates, hampered access to capital, or being locked out of certain transactions. As a supermajority of states belonging to OECD, BRICS, and other major emerging markets move forward with mandatory climate disclosure frameworks (often ISSB-aligned), Canada’s pause of mandatory climate disclosure rules in April 2025 is leaving Canadian companies exposed to cascade pressures without a coherent framework to satisfy them. A single, mandatory reporting framework would improve competitiveness – not hinder it.

Existing securities legislation is not delivering

When the Canadian Securities Administrators paused work on National Instrument 51-107 in April 2025, the rationale was to focus on “initiatives to make Canadian markets more competitive, efficient and resilient,” implying that mandatory disclosure for issuers might not serve that goal. This decision was rationalized by arguing that securities legislation already requires issuers to disclose material climate-related risks “in the same way that issuers are required to disclose other types of material information.” (CSA updates market on approach to climate-related and diversity-related disclosure projects – Canadian Securities Administrators)

There are critical gaps in existing securities legislation, however, that a mandatory climate disclosure framework could fill.

The first gap is who decides what constitutes a material risk. Issuers themselves judge what counts as material, and many conclude that their climate-related risks don’t meet that bar – or don’t clearly spell out these risks when they do. CSA Staff Notices 51-333 (2010) and 51-358 (2019) set out guidance for the disclosure of material environmental and climate-related risks, but this guidance has produced inconsistent and often poor-quality results. In fiscal 2024, the CSA’s continuous disclosure review flagged several qualitative deficiencies specific to climate reporting, including vagueness in terminology, lack of methodological transparency and unsubstantiated ESG claims – all deficiencies that CDSD is designed to address. (The CSA Staff Notice 51-365 – Continuous Disclosure Review Program Activities)

The earlier Climate Change-related Disclosure Project (The CSA Staff Notice 51-354 – Report on Climate Change-related Disclosure Project) found the same pattern. Users, including institutional investors, advocates, rating agencies and analysts, reported climate disclosures were often “boilerplate, vague or viewed as incomplete.” Many concluded that existing securities guidance was not enough, recommending issuers needed to be compelled by specific and clear requirements to provide decision-useful information. The CSA itself concluded that new disclosure requirements should be considered:

“Based on our work in connection with the Project, we believe that new disclosure requirements should be considered in respect of issuers’ governance practices in relation to material business risks and opportunities in general, and their processes for the identification, assessment and management of material risks.” (The CSA Staff Notice 51-354 – Report on Climate Change-related Disclosure Project, page 36)

The notice listed climate change explicitly among the risks the new requirements would address.

Climate disclosures are already required in the ordinary course of business

While the CSA debate continues, the climate disclosure cascade has already reached many Canadian companies through multiple other channels, none of which depend on CSA action. By “cascade” we mean a chain through which a disclosure requirement applying to one institution becomes a data request to its counterparties: the Canadian company isn’t legally bound by the original rule, but the request still arrives.

The OSFI B-15 cascade.

The Office of the Superintendent of Financial Institutions’ Guideline B-15 is currently the only mandatory climate disclosure instrument in force in Canada. It applies to federally regulated financial institutions (FRFIs), i.e. chartered banks, insurers, trust companies. In practice, it reaches much further: any company that borrows from a federally regulated bank, or that is an underwriting client of a federally regulated insurer, is affected.

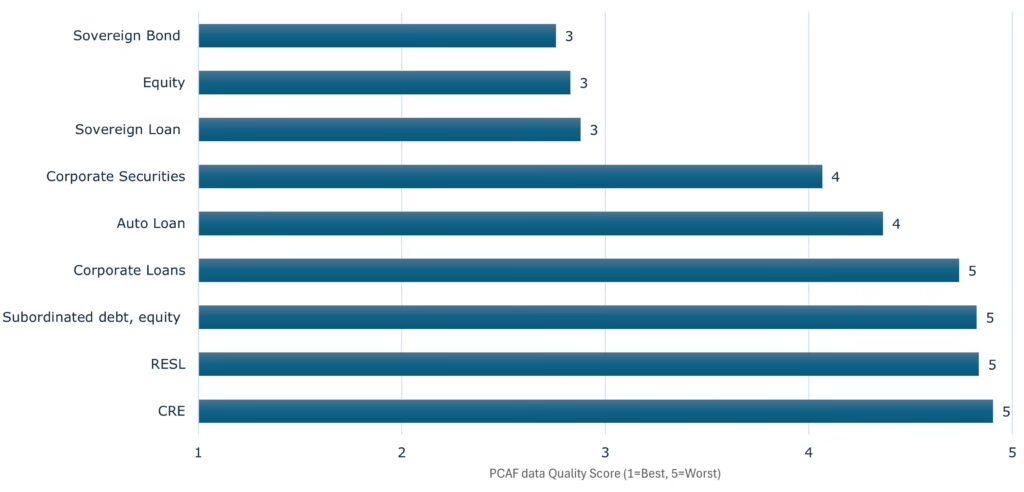

FRFIs must disclose their financed emissions – the share of their borrowers’ and clients’ emissions that can be attributed to the financing they’ve provided. To do this, they use the PCAF (Partnership for Carbon Accounting Financials) Standard, which assigns a 1-to-5 quality score to each counterparty’s emissions data. A score of 1 means the counterparty has provided audited emissions data. A score of 5 means the FRFI had to use an estimate based on sector and regional averages instead of real counterparty data. OSFI’s own stated goal is “to progress over time from proxy-based estimates toward more reliable, counterparty-specific data”. (Insights from the 2025 Climate Risk Returns)

The requirements are set to expand. By fiscal year 2028, FRFIs must publish Scope 3 financed emissions – the full chain of indirect emissions across their lending and underwriting books. By fiscal year 2029, the cascade extends to issuers of capital markets instruments the bank helped bring to market, even without a direct lending relationship. In other words, almost every Canadian company that has issued securities through a Canadian bank-affiliated dealer becomes part of the picture.

Estimated climate data can be wildly off for clean producers. A modern primary aluminum smelter in Quebec running on hydroelectricity emits roughly 1.6 tonnes of CO₂-equivalent per tonne of aluminum produced (Rio Tinto to expand its AP60 low-carbon aluminium smelter in Quebec | Global). The global industry average, published by the International Aluminium Institute, was 14.8 tonnes per tonne – over nine times higher (Aluminium, primary production – Carbon Footprint Platform – OpenCO2.net). A Quebec smelter that doesn’t disclose appears in its bank’s books closer to the global-average number than to its real one.

Best-in-class companies – efficient producers, clean-grid operators, and companies using advanced production routes – all face the same problem: the proxy overstates their emissions, and the bank’s reported portfolio looks dirtier than it is.[1] If they voluntarily provide CSDS-aligned disclosures, they face additional costs not borne by their lower-performing counterparts. The lack of an across-the-board climate disclosure requirement, in other words, punishes the best performers.

The EU CSRD cascade.

The EU’s Corporate Sustainability Reporting Directive (CSRD) remains one of the most ambitious climate disclosure regulations globally, even after it was modified by Omnibus I, in force as of 18 March 2026. Under the new Article 40a thresholds, a non-EU group falls into scope only if its ultimate parent generates more than €450 million in EU net turnover for two consecutive years AND has either an EU subsidiary above €200 million in net turnover or an EU branch above €50 million (EUR-Lex – 02022L2464-20260318 – EN – EUR-Lex).

Before the Omnibus, Global Affairs Canada estimated that approximately 5,000 Canadian companies were in scope of the CSRD. Guide to EU sustainability reporting and due diligence – Tradecommissioner.gc.ca The European Commission estimates Omnibus I has now reduced CSRD scope by roughly 90 percent globally (Agreement on the CSRD/CS3D Omnibus Package: key changes and implications), which would put the post-Omnibus Canadian population somewhere around 500 groups (parents and their consolidated subsidiaries) – those with the largest EU operations. No updated Canadian-government estimate has been published. PwC Canada notes that many Canadian companies are still surprised to discover they fall within scope, particularly those with EU-listed securities, large EU subsidiaries, or EU holding company structures (Navigating CSRD | PwC Canada).

Even at this narrower scope, Canadian groups in scope must publish a sustainability report at the level of the third-country parent – the obligation cascades from the EU subsidiary up to the Canadian parent under Article 40a. (EUR-Lex – 02022L2464-20260318 – EN – EUR-Lex) Smaller Canadian suppliers to CSRD-reporting companies will continue to face downstream data requests, although the EU has now introduced a “value-chain cap” protecting partners with fewer than 1,000 employees. (Guide to EU sustainability reporting and due diligence – Tradecommissioner.gc.ca)

The California cascade.

Starting on August 10, 2026, U.S.-organized entities with global revenues above USD $1 billion that do business in California must publicly disclose their Scope 1 and Scope 2 GHG emissions under SB 253 (the Climate Corporate Data Accountability Act). Scope 3 reporting begins in 2027. CARB’s preliminary list identifies about 2,000 entities directly subject to SB 253 and a further 1,500 subject only to SB 261, predominantly large US-headquartered companies in technology, retail, energy, financial services, and manufacturing.[2] (Harvard Law School Forum on Corporate Governance, October 2025) Penalties under SB 253 reach $500,000 per reporting year.

The direct cascade to Canadian companies is currently narrow: only two Canadian-jurisdiction entities appear on CARB’s preliminary list – The Toronto-Dominion Bank and TFG Financial Corporation. Most large Canadian groups with material California business operate through US-incorporated subsidiaries, which appear on the list under their US names. While the legal reporting obligation falls on the US subsidiary, the data-collection effort and value-chain pressure run back to the Canadian parent. (California Air Resources Board Approves Initial Regulations for SB 253 and SB 261 | Sullivan & Cromwell LLP)

The indirect cascade, through Scope 3 reporting starting in 2027, is far broader.

From 2027, each of the roughly 2,000 SB 253 reporters will need Scope 1 and 2 emissions data from suppliers across their value chains to compile their own Scope 3 disclosures.[3] (CARB’s SB 253 Workshop: Initial Reporting and the Road to Scope | Akin, The hidden cost of Scope 3 — Why SB 253 could reshape supplier relationships forever | UL Solutions) Canadian companies supplying components, raw materials, services, or finished goods to large US firms will face the same dynamic seen with OSFI B-15: not a legal obligation in Canada, but a commercial one from customers who now need the data.

SB 261 (the Climate-Related Financial Risk Act), whose enforcement was paused by a Ninth Circuit injunction in November 2025, imposes biennial climate-risk disclosure on companies above $500 million in global revenue doing business in California. “Doing business in California” is triggered by California sales above $735,019 in 2024, property or payroll above set thresholds, or any commercial activity in the state. (California Climate Disclosure Rules for Non‑U.S. Companies)

The CBAM cascade.

The EU’s Carbon Border Adjustment Mechanism (CBAM) entered its definitive phase on January 1, 2026; the UK CBAM follows on January 1, 2027. CBAM attaches a carbon cost – €75.36 per tonne of CO₂e in Q1 2026 – to imports of cement, iron and steel, aluminium, fertilizers, electricity, and hydrogen, with downstream products under EU consideration (Carbon Border Adjustment Mechanism – Taxation and Customs Union). The legal obligation falls on EU importers, but importers need verified product-level embedded-emissions data from their suppliers, calculated to EU methodology and audited by an accredited verifier. Where that data isn’t provided, EU default emission values apply – and those defaults carry a mark-up that raises over time, from 10% in 2026 to 20% in 2027 and 30% in 2028. (Commission Implementing Regulation (EU) 2025/2621 of 16 December 2025 laying down rules for the application of Regulation (EU) 2023/956 of the European Parliament and the Council as regards the establishment of default values)

The defaults work the same way PCAF proxies do under OSFI B-15: where countries haven’t provided reliable data, the EU sets the default at roughly the dirtiest reliable producer’s intensity. For unwrought aluminium, that’s around 3 tonnes of CO₂-equivalent per tonne[4][5] – roughly twice the 1.6 tonnes per tonne emitted by a Quebec hydroelectric smelter. A Canadian smelter that doesn’t disclose pays CBAM as if it were a Chinese coal-powered facility; one that does disclose pays about a tenth as much. The structural asymmetry isn’t accidental: the default is designed to under-count dirty producers (who get a discount by relying on it) and over-count clean producers (who get penalized for not proving their advantage).

Most Canadian aluminium and steel currently goes to the US, not the EU. But as Canada accelerates trade diversification toward Europe and other middle powers, CBAM exposure will grow. The stakes are higher because the affected Canadian sectors happen to be among the cleanest globally:

- Canadian aluminium has by far the lowest carbon footprint of any major producer (hydroelectric smelters in Quebec and BC) (Canada Aluminum Exports & CBAM Advantage In 2025);

- Canadian steel is among the lowest-carbon globally (electric arc furnaces on clean Ontario and Western grids) (Steel Climate Impact 2022 – An International Benchmarking of Energy and CO2 Intensities — Global Efficiency Intelligence);

- Canadian ammonia has the lowest net emissions intensity of any country in Fertilizer Canada’s 2023 benchmarking.

Without verified data audited to EU standards, Canadian exporters can’t claim that advantage – they get the default plus mark-up instead.

Beyond these four cascades, a more diffuse fifth one runs through Canadian companies’ international lenders, insurers, and reinsurers. Under the EU’s Capital Requirements Regulation (CRR3), all EU banks are required to disclose financed emissions and ESG risks in their lending books from 2025 (pwc-whitepaper-crr-3-to-go.pdf), with expanded Pillar 3 ESG templates applying from December 2026 (Transparency and Pillar 3 | European Banking Authority). Under the UK Prudential Regulation Authority’s Supervisory Statement 5/25 (in force since December 2025), UK banks, insurers, and Lloyd’s of London managing agents must manage and disclose climate-related risks across their books (PS25/25 – Enhancing banks’ and insurers’ approaches to managing climate-related risks – Update to SS3/19 | Bank of England, ClimateWise – Lloyd’s).

PCAF Part C, the global insurance-associated-emissions standard (updated in December 2025 to cover treaty reinsurance) captures some major reinsurers used by Canadian companies, including Swiss Re, and Hannover Re. The pattern is the same as B-15: data requests cascade from regulated financial counterparties to their Canadian clients, regardless of the client’s own size or listing status.

The data we’re getting from the patchwork is poor

Even on the channel that is mandatory and running – OSFI B-15 – the data quality picture is sobering. OSFI’s Insights from the 2025 Climate Risk Returns shows that for systemically important domestic banks, PCAF data quality scores are frequently worst-in-class (See Figure 4). (Insights from the 2025 Climate Risk Returns)

Figure 4 – Average PCAF data quality score (D-SIBs)

Where a counterparty’s actual emissions are lower than the sector-and-regional average – efficient producers, operations on clean grids, facilities using advanced production routes – proxy-based estimates over-count them in their lender’s published figures. That creates a specific commercial incentive for those companies to disclose: their actual data, even if imperfect, is likely better than the proxy (Benchmarking Methane and Other Greenhouse Gas Emissions 2024 | Ceres: Sustainability is the bottom line). Worst-in-class companies feel no such incentive – and face no such costs.

The corresponding pressure from the insurance and investor sides is real but largely prospective. Insurers have the levers – premium pricing, deal terms, refusal to insure – to push underwriting clients toward better data, and several have stated long-term sustainability goals that depend on counterparty data quality, including Intact and Manulife. Pension funds, which fall outside OSFI B-15, have their own levers: selective engagement with companies that disclose, divestment or reallocation from those that don’t. UPP’s Climate Stewardship Plan and La Caisse’s 2025–2030 climate strategy are examples of this approach being formalized. How aggressively these levers will be used at scale remains to be seen.

One rulebook would be lighter, not heavier

Put together, the picture is this: A Canadian company today may face climate disclosure requests from its Canadian or international lender (OSFI B-15 / PCAF), its insurer (PCAF Part C, mandatory from 2028), its pension-fund investors, its EU customers or parent (CSRD/CBAM), and/or its California-based customers (SB 253 from 2027). On top of that sits the inconsistent material-risk disclosure CSA continuous disclosure reviews keep flagging as deficient. The reporting burden compounds across overlapping but non-aligned frameworks.

A single mandatory framework – CSDS 1 and CSDS 2, already ISSB- and IFRS S1/S2-aligned – would let one report serve multiple regulators, lenders, investors, customers, and supervisors. It would raise data quality. It would reduce ad-hoc demands. And it would bring Canada into line with the supermajority of OECD, BRICS, and other major economies already on this path.

The original reason for pausing NI 51-107 was to make Canadian markets more competitive, efficient, and resilient. One year later, the evidence suggests the pause is achieving the opposite. As Canada pivots toward diversified trade and a more resilient capital market, resuming work on mandatory climate disclosures – through the CSA, through CBCA amendments, or both – is one of the lower-cost, higher-leverage moves available.

Let Canadian companies report once, well, and to a standard in use throughout most of the world.

Click the footnote to return to the article section.

[1] PCAF’s specific physical-activity emission factors are published in the PCAF Database, which is accessible only to signatory institutions (banks, insurers, and asset managers who have signed the PCAF commitment). However, these factors are derived from publicly available sources. The figures cited here are from those underlying public sources rather than from the restricted database itself. A bank applying PCAF’s physical-activity methodology to a non-disclosing aluminum borrower would use a similar global or regional sector-average factor, with the specific value depending on which regional cell the institution selects.

[2] CARB Preliminary List of Reporting/Covered Entities, posted September 24, 2025: 4,161 total entries covering 3,127 unique entity names, of which 2,596 are flagged for both SB 261 and SB 253 and 1,564 for SB 261 only. Only 2 unique Canadian-jurisdiction entities appear on the list (TD Bank, TFG Financial Corporation). Most large Canadian companies with California business appear on the list under their US-incorporated subsidiaries’ names. CARB notes the list is preliminary and not a definitive scope determination. https://ww2.arb.ca.gov/sites/default/files/2025-09/SB%20253_261_preliminary_list_092425.xlsx

[3] The reporting and assurance obligations under SB 253 sit with the U.S. customer, not the supplier. Canadian suppliers face no direct California requirement to verify the data they provide or follow a particular standard. Commercial preference for verified, GHG Protocol-aligned data will increase over time as customers face their own assurance obligations and the GHG Protocol’s 2026 Scope 3 revisions introduce new data-quality labelling.

[4] EU default values for unwrought aluminium include China at 3.0 tCO₂e/t (Scope 1), India and UAE at 1.87 tCO₂e/t. Canada is not separately listed; under the Omnibus regulation, defaults for countries without reliable data are set at the highest emission intensity observed among countries with reliable data for the respective product. Reported by Argus, “EU lowers CBAM benchmarks for aluminium” (11 Dec 2025). https://www.argusmedia.com/en/news-and-insights/latest-market-news/2764083-eu-lowers-cbam-benchmarks-for-aluminium

[5] PCAF reflects a producer’s full footprint including electricity; CBAM mostly captures direct process emissions. That’s why the over-attribution gap looks larger under PCAF. The structural dynamic – defaults penalizing clean producers who haven’t proved their advantage – is the same.